Surety Bond FAQS

Why Do I Need a Surety Bond?

You may be legally required to purchase a surety bond due to your job type or where you work. Many government agencies mandate surety bonds for certain industries or business licenses as a preventative measure for consumer protection.

What Does a Surety Bond Cover?

Surety bonds protect government entities, businesses and consumers from loss by holding bonded parties financially liable for their legal obligations. If the bondholder breaches the contract terms, harmed parties can recover their loss by filing a claim on the bond.

Types of bond obligations can range from completing a contracted project to following industry licensing rules to properly managing estate assets.

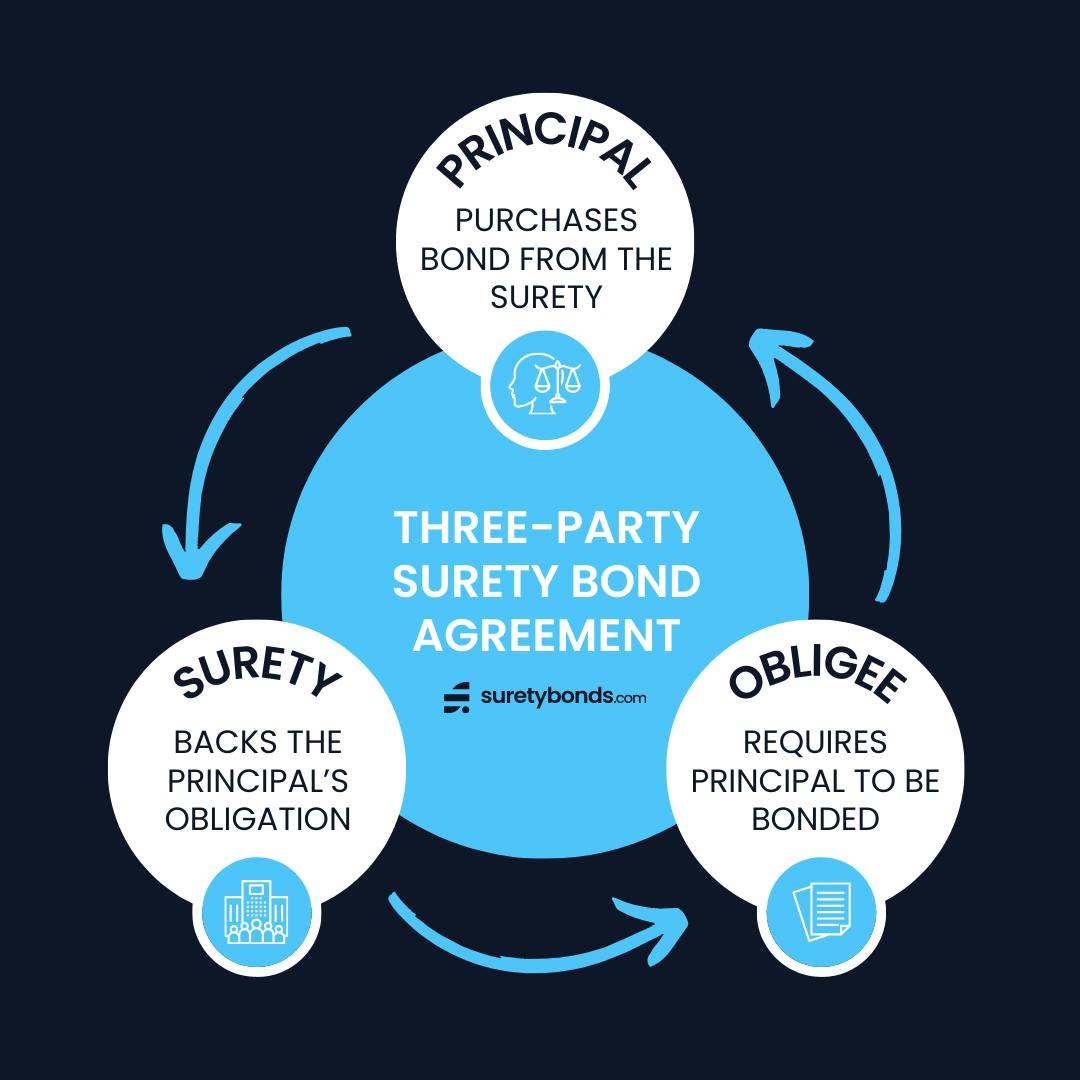

Who Is the Principal in a Surety Bond Contract?

Each surety bond joins three parties in a legally-binding contract: the principal, the obligee and the surety provider.

If you are purchasing the bond, you are the principal. The obligee is typically a government entity that requires the bond. The principal must file the bond with the obligee and comply with their terms.

Where Can I Get a Surety Bond?

You can purchase a surety bond online from a licensed surety provider. Simply apply for a quote online, pay for your bond and file it with the obligee.

SuretyBonds.com is licensed to issue bonds in all 50 states

How Much Does It Cost to Get a Surety Bond?

The cost of a surety bond ranges between 0.5 to 10% of the bond amount in most cases. Some bonds cost a set premium for every applicant. However, underwritten bond premiums are calculated based on the amount of coverage, bond risk and the principal’s financial history.

A bond’s jurisdiction could also affect your surety rate. For more local pricing information, select your state below:

Does It Cost to Apply for a Bond?

No, the surety bond application process is completely free! Apply today and receive a quote within one business day—or instantly for certain bonds.

Secure | No Obligation | Takes 2 Minutes

When Do I Have to Pay for My Surety Bond?

Surety providers almost always require full upfront payment before they issue a bond. Most companies accept credit/debit cards for quick payment online or over the phone.

What Bond Amount Do I Need?

Bond amounts are typically determined in one of two ways:

- Fixed Amounts: The bond amount is the same for all clients.

- Ranged Amounts: The bond amount varies depending on the client's license type, business volume, vehicle value, scope of obligation, etc.

Bond coverage requirements are set by the obligee, the party requiring the bond. Contact your obligee to determine the exact bond amount you need.

How Are Surety Bonds Different From Insurance Policies?

Bonds and insurance policies are separate means of financial protection:

- Insurance is a risk-transfer tool between two parties where individuals exposed to similar risks contribute premiums into a pool.

- Surety bonds act as risk-mitigation contracts between three parties where financial loss is not expected.

Insurance policies act as a retroactive protection, while bonds function more like a line of credit. Read more about standard insurance vs “surety insurance.”

What Is a Letter of Credit vs a Surety Bond?

Surety bonds and letters of credit are both forms of financial guarantees, but they are not the same thing:

- A letter of credit is issued by a bank to assure a seller they will receive payment from a buyer.

- A surety bond does not require a line of credit and is issued by an insurance provider to guarantee performance of contractual obligations.

What If I Don’t Have a Final Business Name or Address?

You don’t need a final business name or address to apply for a bond with SuretyBonds.com. You should, however, have a professional business name and address before submitting payment.

What If I Need to Change the Information on My Bond?

You cannot alter your bond forms without submitting the change request to your provider. If you need to change information on your bond, gather answers to these questions:

- Has the bond been filed?

- What is the exact change needed?

- Have you spoken with the obligee to verify if they have any specific instructions regarding the change?

- Is the obligee requiring a new bond, or will they accept a change "rider" document?

- When does the change need to go into effect?

Next, call 1 (800) 308-4358. One of our friendly representatives will be happy to help approve and issue your bond updates.

What Is a Bond Rider?

For certain bond changes, you may receive a bond rider. A rider is a document attached to an active surety bond that indicates an information change from the original bond form. Common rider change requests include:

- Legal names

- Business addresses

- Bond terms

- Bond amounts

Riders must always be filed with the obligee.

Which Surety Bond Company Should I Choose?

When selecting the best surety provider to get your bond from, look for these attributes:

- Reputable: Verify if the company has several years of industry experience and positive reviews.

- Licensed: Confirm if they offer the bond coverage you need and are licensed to do business in your state.

- Helpful: Look for a provider offering live customer support and friendly service.

- Affordable: Check if the company offers competitive rates and whether they charge any fees. If you have low credit, you’ll also want to look for bad credit bonding programs.

Why Choose SuretyBonds.com?

We’ve been around since 2014 and are the industry leaders in creating a fast, easy and affordable bonding process. SuretyBonds.com is:

- Licensed in all 50 states

- Available Mon–Fri with friendly customer support 7 am–7 pm

- Backed by over 12,000 5-star customer reviews

As an agency, we provide the most competitive rates using our network of providers. Plus, we charge zero brokerage fees, provide free quotes and offer bad credit bond approval options.